Pay Rent with Stablecoins: Landlord Accounting + UX Realities

In early April 2026, UrbanPay published a compliance guide showing that the EU's MiCA regulation and the US GENIUS Act together create the first coherent framework for stablecoin use in commercial real estate transactions — including rent. The guide notes that receiving stablecoins in exchange for rent is a taxable event in both jurisdictions, that EU DAC8 reporting begins on data collected from January 1, 2026, and that IRS Form 1099-DA requires reporting of digital asset transactions by brokers and exchanges starting in 2026. For a CFO evaluating whether to accept stablecoin rent payments, the technology is no longer the bottleneck. The bottleneck is the accounting, tax reporting, and banking partner acceptance that sit behind the payment.

The Legacy Workflow

A tenant pays rent by ACH transfer, wire, or check. The landlord's property management software records the payment against the lease. The bank processes the deposit within 1 to 3 business days for ACH, same-day for wire. Tax reporting is straightforward because the payment is denominated in local currency and the bank provides the records.

The pain points are cross-border friction, settlement timing, and banking access. An international tenant sending rent via wire pays 25 to 50 dollars in fees plus an FX spread. ACH takes 1 to 3 business days. And tenants without local bank accounts — common for digital nomads and international professionals — may not be able to initiate the payment at all.

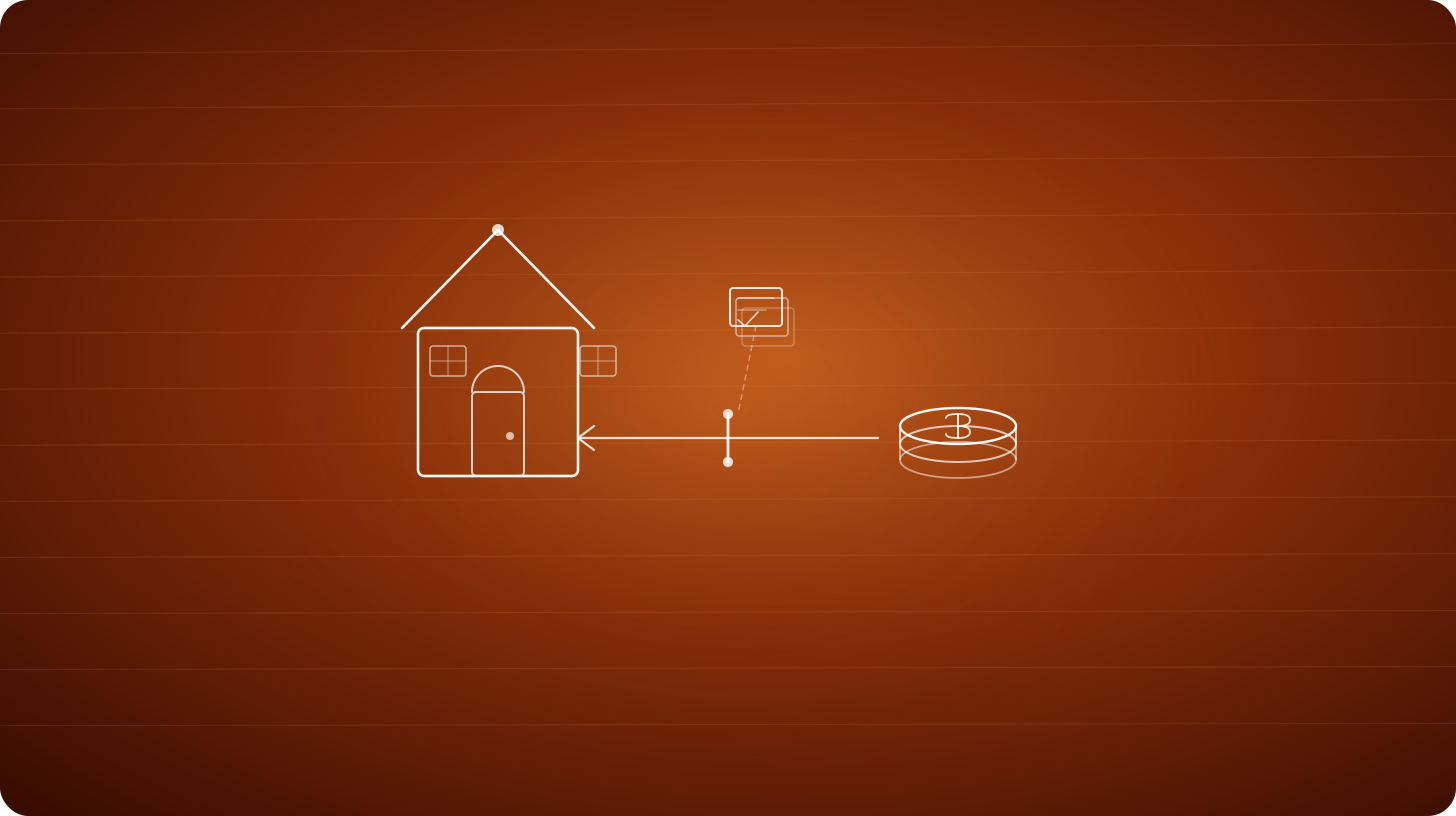

The Stablecoin Workflow

A tenant holds USDC, USDT, or EURC in a self-custodial wallet and sends the stablecoin amount matching the lease denomination to the landlord's designated address or through a settlement bridge like TrustLinq, which converts to local fiat and delivers a standard bank transfer. The landlord never touches crypto. Settlement follows traditional rails: SEPA for EUR, Faster Payments for GBP, ACH for USD.

The alternative is the landlord accepting stablecoins through a payment processor. Jamestown, a global real estate firm managing approximately 26 million square feet, partnered with BitPay in 2022 to accept crypto rent payments across its US portfolio, with BitPay converting to fiat before the landlord receives funds. The landlord does not hold the digital asset.

In both models, the tenant experience improves: payment initiates instantly from any jurisdiction, settles within minutes on-chain, and does not require a local bank account. The friction appears only when the landlord tries to hold stablecoins on their balance sheet rather than converting immediately.

Where the Accounting Breaks

Three accounting problems arise the moment a property company receives stablecoins rather than converting immediately. First, revenue recognition. If the landlord receives 2,000 USDC for rent and the USDC peg holds at exactly one dollar, the revenue is 2,000 dollars. But if the peg fluctuates even slightly between receipt and conversion, there is an FX-like gain or loss that must be tracked. The UrbanPay guide is direct: holding stablecoins on your balance sheet introduces foreign-exchange-like tracking complexity that most property companies should avoid.

Second, tax reporting. In the US, the IRS treats stablecoins as digital assets. Receiving USDC as rent is a taxable event at fair market value on the date of receipt. Starting in 2026, Form 1099-DA requires brokers and exchanges to report these transactions. If the landlord converts stablecoins to fiat immediately upon receipt within the same transaction, the tax position is straightforward and functionally identical to receiving a dollar payment. In the EU, DAC8 requires crypto-asset service providers to begin collecting transaction data on EU-resident users from January 1, 2026, with first reporting due by September 30, 2027.

Third, banking partner risk. A property company's bank evaluates the company's risk profile. Receiving crypto-related deposits, even if converted to fiat through a regulated bridge, can trigger enhanced due diligence from the bank. If the bank decides the crypto exposure exceeds its risk appetite, the property company can lose its banking relationship — the same risk that fiat on-ramp providers face at a structural level.

What Is Improving and What Breaks First

The constructive signal is regulatory clarity. MiCA classifies dollar-pegged stablecoins as e-money tokens requiring banking-grade licenses and full reserves. Circle's USDC has an EMI license through Ireland. The GENIUS Act establishes the first US federal framework for stablecoin issuance. Together, these give banks a compliance basis for accepting stablecoin-derived deposits. The FDIC's April 7 proposed rulemaking under the GENIUS Act explicitly addresses custody and reserve standards.

What breaks first is the landlord's banking relationship. The earliest detection signal is the bank asking new questions about the source of funds or requiring additional documentation for stablecoin-converted deposits. The second failure point is the tenant's off-ramp: if the settlement bridge loses its own banking relationship, the fiat leg fails even though the on-chain leg succeeded. The metric proving adoption is accelerating would be property management platforms integrating stablecoin payment rails natively. That number is small but growing as platforms like Rent.App add USDC and USDT options with zero-fee conversion.

For informational purposes only. Not an offer to buy or sell any security. Available only to accredited investors who meet regulatory requirements.