When to Hold Crypto vs Convert Immediately: The CFO Framework

In June 2026, Kyriba — whose platform manages more than 3.6 billion bank transactions and 51 trillion dollars in payments annually — announced stablecoin treasury integration work with Ledger and Mantu, powered by Fipto handling conversion, settlement, and compliance monitoring in the background. On February 17, 2026, Payoneer announced stablecoin capabilities powered by Bridge, a Stripe company, letting businesses receive, hold, and send stablecoins from Q2 2026 inside the payment account they already use. Circle launched CPN Managed Payments on April 8. PayPal settles merchants directly in USDC. As one analysis put it, once stablecoins enter the enterprise treasury platform, the conversation becomes treasury policy, not crypto ideology. The policy question every CFO now owns: when a payment arrives in crypto, do you hold it or convert it immediately? The answer is a framework, not a preference — and the CFO already has the template, because it is the FX receipts policy applied to a new currency class.

The Legacy Workflow

A company receiving foreign-currency payments does not improvise. The FX policy defines it: operating thresholds per currency, conversion triggers, netting of receipts against payables in the same currency, and hedging for net exposure above a band. Receipts in a currency the company also spends stay in that currency to avoid paying the conversion spread twice; receipts with no matching outflow convert on a schedule. The treasury committee sets the policy, the TMS executes it, and the auditor tests receipts against it. Crypto receipts have mostly bypassed this discipline — routed through a processor that auto-converts everything to fiat by default, or worse, accumulating in a wallet with no policy at all, making someone an accidental crypto treasurer.

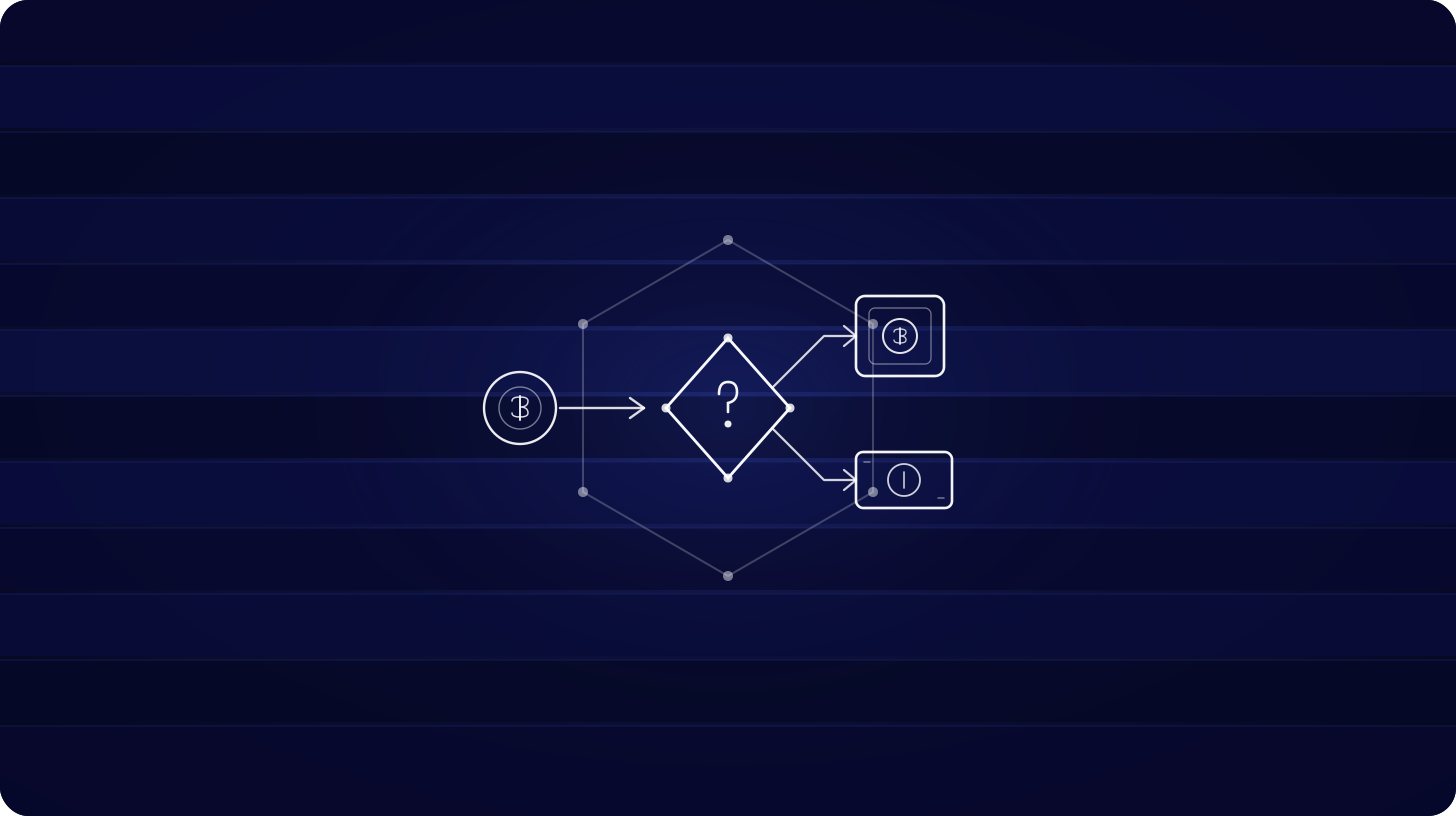

The Decision Framework

The framework splits on asset class first. Volatile crypto (BTC, ETH) received as payment converts immediately by default. The reasons are mechanical: working capital has a volatility budget of zero; ASU 2023-08 fair-value accounting marks holdings through net income every period, importing price swings into reported earnings; and every later disposal is a taxable event requiring lot tracking. If the company wants BTC on the balance sheet, that is a board-approved treasury allocation decision with its own mandate, custody, and sizing — made deliberately, never as a byproduct of accounts receivable.

Stablecoins are the genuine decision. The test is the match ratio: what share of the company's outflows can be paid in the received stablecoin? A marketplace paying 400 overseas contractors 300,000 dollars monthly in USDC should hold incoming USDC up to an operating buffer sized to those outflows — auto-converting to fiat and re-converting to pay contractors pays the conversion spread twice for no reason. The published economics make the point: managed stablecoin payout flows run roughly 0.5 percent all-in (1,500 dollars on that 300,000), against 6,000 dollars in wire fees alone before FX spread. A company with purely fiat outflows inverts the answer: convert stablecoin receipts on receipt, because an idle stablecoin balance earns nothing — GENIUS-compliant payment stablecoins cannot pay yield — while carrying issuer and depeg exposure. Balances above the operating buffer follow the two-product pattern: convert, or move to a tokenized money market sleeve as a deliberate investment position with its own accounting, never left idle in the payment wallet.

Where the Plumbing Breaks

Three failure points define the workflow. First, policy absence: receipts accumulate ad hoc, the company discovers it holds six figures of volatile crypto with no mandate, and the write-down arrives with the audit. The fix is a routing policy the payment orchestrator enforces automatically — hold, convert, or sweep, decided per asset class before the first payment arrives. Second, the double-spread round trip: default auto-conversion looks conservative but silently costs two spreads whenever the company has stablecoin-denominated outflows. Third, the off-ramp bottleneck: crypto settles continuously, but fiat conversion has banking cutoffs, weekend gaps, and counterparty limits — a treasury that assumes instant convertibility at size discovers the conversion leg, not the blockchain leg, is the constraint.

Costs, Timing, and the Audit Trail

The conversion decision now executes in seconds through platforms offering optional auto-conversion on payment links, named EUR and USD IBANs, and segregated stablecoin wallets — against one-to-three-day correspondent settlement on the legacy rail. For a CPA evaluating the audit trail, the evidence chain is the policy applied per receipt: the treasury policy document defining thresholds and exception approvals; the routing engine's timestamped decision log per payment (held, converted, swept); conversion confirmations showing spread against mid; wallet balances reconciled monthly to the general ledger by entity; fair-value marks under ASU 2023-08 for any volatile holdings; tax lots for every disposal; and reliance on the stablecoin issuer's reserve attestation for held balances. The reconciliation tests receipts against policy the same way it tests FX receipts. The constructive signal is that the hold option itself is going mainstream — when Payoneer, PayPal, and the largest treasury management platform all ship receive-hold-send capability in the same year, holding is no longer an operational improvisation but a policy choice with enterprise-grade rails, and EY's projection of 2.1 to 4.2 trillion dollars in stablecoin cross-border volume by 2030 says the decision will only get more frequent.

For informational purposes only. Not an offer to buy or sell any security. Available only to accredited investors who meet regulatory requirements.