Compliance Wallet Flow: Whitelist, Restrictions, Reporting

On March 4, Kraken Financial became the first digital asset bank to receive a Federal Reserve master account, giving it direct access to Fedwire settlement without intermediary correspondent banks. The approval, initially for one year, means a Wyoming-chartered crypto institution now connects to the same payment rails as traditional banks. For a compliance officer evaluating how regulated digital assets actually move, this milestone illustrates the endpoint: a fully compliant entity settling fiat and crypto on integrated infrastructure. The less visible but equally critical question is what happens upstream, inside the on-chain compliance workflow that determines whether a wallet is allowed to hold, send, or receive a regulated token in the first place.

The Legacy Workflow

In traditional securities, compliance controls are enforced by intermediaries. A broker-dealer verifies investor identity during account opening, a transfer agent maintains the shareholder registry, and a custodian holds the assets. A typical cross-border securities transfer involves KYC checks at the broker, sanctions screening at the custodian, and regulatory reporting at the transfer agent, each operating on its own timeline and system. The process works, but it is slow, expensive, and opaque.

The On-Chain Workflow

When a tokenized security is issued under a compliance-aware standard like ERC-3643, the workflow collapses these intermediary functions into smart contract logic. The process follows a specific sequence.

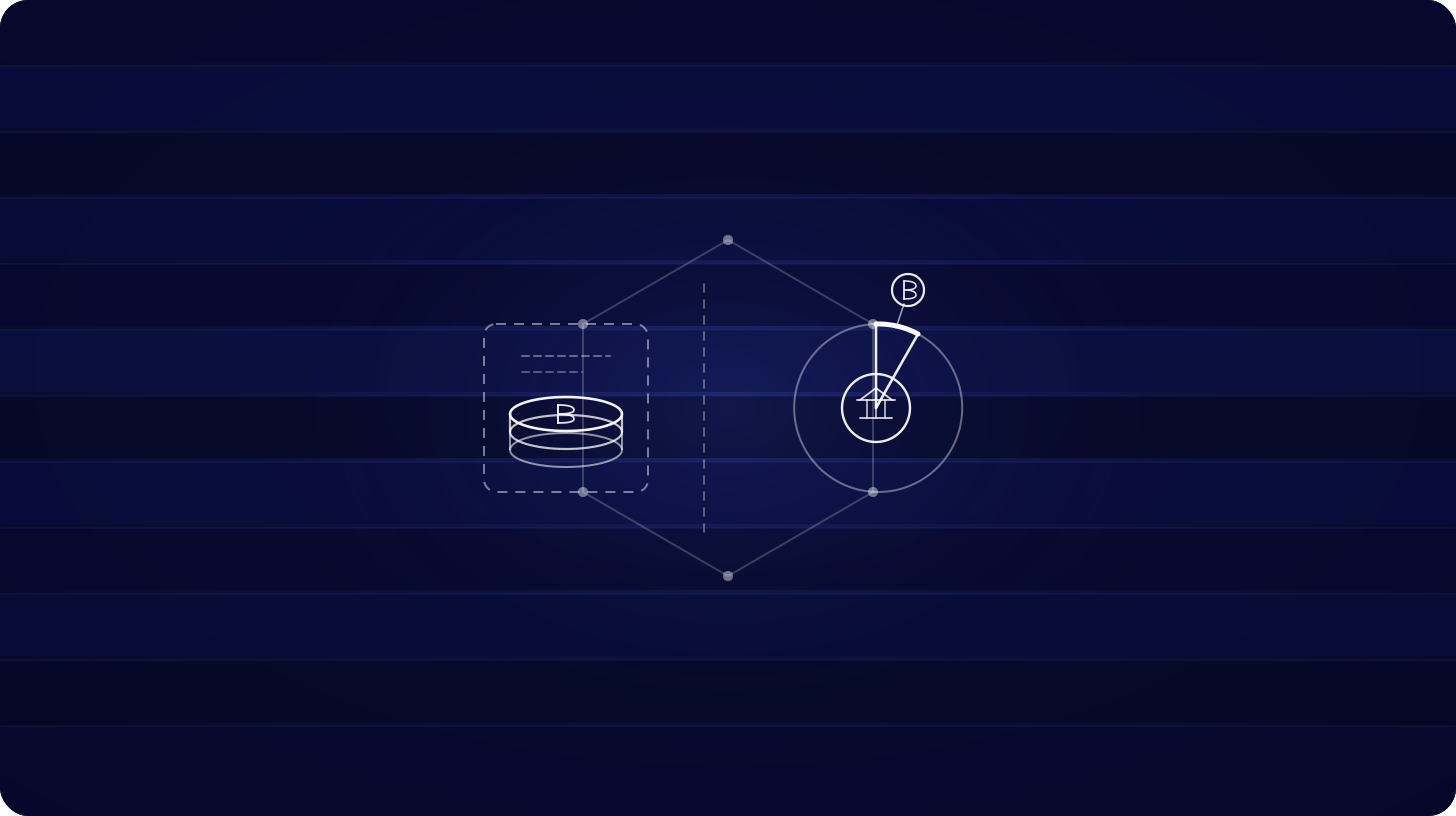

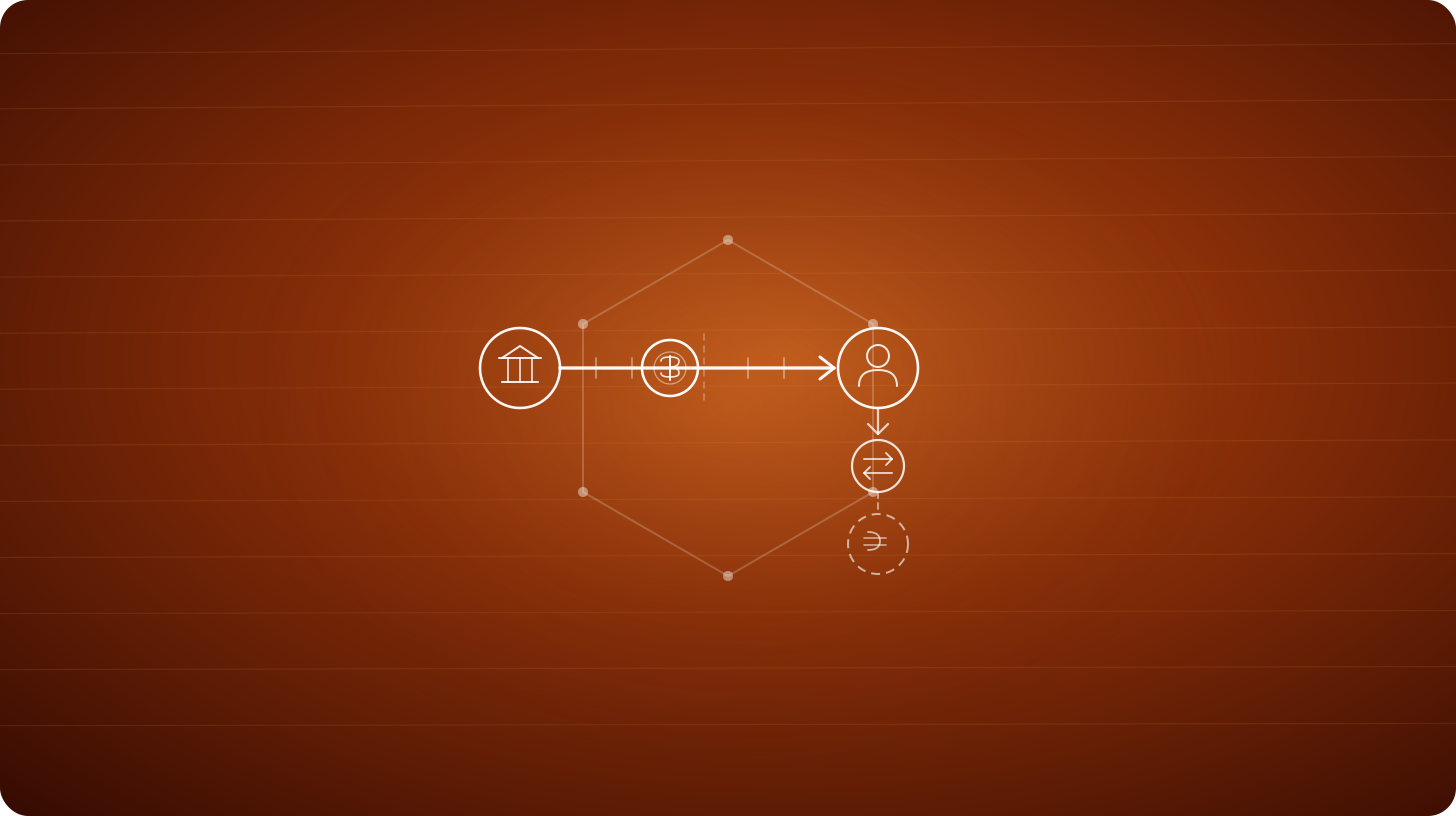

First, the investor completes KYC and accreditation verification off-chain. Upon passing, a cryptographic identity credential is linked to their wallet address in an on-chain identity registry. This credential attests that the wallet belongs to a verified individual meeting specific requirements, such as accredited investor status or sanctions clearance, without exposing personal data on the public blockchain.

Second, the issuer whitelists the wallet address by adding it to the token's transfer restriction logic. The smart contract maintains an allowlist of approved addresses. Only wallets on this list can receive the token. When a transfer is attempted, the contract checks both the sender and receiver against the registry before executing.

Third, transfer restrictions enforce ongoing compliance automatically. The contract can block transfers to restricted jurisdictions, prevent holdings from exceeding concentration limits, enforce minimum holding periods, and verify that the receiver's credential has not expired. If any condition fails, the transfer reverts.

Fourth, reporting happens natively. Every successful and rejected transfer is recorded on the blockchain with a timestamp, the addresses involved, and the outcome. This creates an immutable audit trail that regulators can query without requesting reports from multiple intermediaries.

What Improves

The operational gains are measurable. Transfer settlement drops from T+2 to seconds. Reconciliation burden falls because the ledger is shared: issuer, investor, and regulator all reference the same record. Compliance verification moves from post-trade to pre-trade, preventing violations rather than detecting them after the fact. And the audit trail is continuous rather than reconstructed from fragmented records during examinations.

The GENIUS Act's OCC rulemaking, published March 2, requires that stablecoin issuers maintain enforceable redemption rights and segregated reserves. The SEC's 2 percent haircut ruling for broker-dealers holding GENIUS-compliant stablecoins treats them as functionally equivalent to money market funds for capital purposes. These regulatory developments are creating the conditions where compliant wallets become the standard interface between on-chain assets and traditional settlement infrastructure.

Where It Breaks

Three friction points limit adoption. First, KYC credential portability. Each issuer currently maintains its own identity registry. An investor whitelisted for one tokenized fund must re-verify for another, even if both use the same KYC provider. Cross-issuer credential standards like Chainlink's Cross-Chain Identity framework are emerging but not yet widely adopted.

Second, the UX gap. Connecting a wallet to a compliance registry, maintaining credential freshness, and understanding why a transfer was rejected are not intuitive for most users. The EU's Transfer of Funds Regulation requires CASPs to verify ownership of unhosted wallets for transfers above 1,000 euros, adding friction that does not exist in traditional account-based systems.

Third, liquidity fragmentation. A token that can only transfer between whitelisted addresses has a smaller tradable universe than one that circulates freely. This restricts secondary market depth, widens spreads, and limits price discovery. Permissioned DeFi venues where all participants are pre-verified attempt to solve this, but they sacrifice the composability that makes public DeFi valuable.

What a Pension Allocator Needs to See

For a pension fund or family office to approve exposure, the compliance workflow must demonstrate four properties: identity verification meeting existing custodian standards, automatically enforced transfer restrictions, an audit trail exportable in formats auditors accept, and reliable redemption under stress. Kraken's Fed master account shows the settlement layer is converging. The compliance wallet workflow shows the access control layer is maturing. The gap is in the middle: standardized credential portability and institutional-grade UX that makes on-chain compliance invisible rather than burdensome.

For informational purposes only. Not an offer to buy or sell any security. Available only to accredited investors who meet regulatory requirements.