Privacy Primitives Institutions Can Actually Use Slug

The institutional privacy problem is not anonymity — it is confidentiality with selective disclosure. A bank settling on a public ledger cannot let competitors read its counterparties, volumes, and positions, but it also cannot adopt a tool that hides those flows from its own auditors and regulators. The post-Tornado Cash regulatory logic is precise: anonymity that cannot be selectively lifted is the target, not confidentiality itself. The Fifth Circuit's November 2024 ruling drew the boundary — sanctions law reaches people and entities, not autonomous code. By 2026, the primitives that thread this needle are in production. The Canton Network has processed more than 4 trillion dollars in on-chain real-world asset volume using sub-transaction selective disclosure. For a technical PM evaluating which privacy primitive an institution can actually deploy, the test is whether a banking examiner's questions have clean answers.

The Architecture and Trust Model

Four primitives carry institutional weight. Zero-knowledge proofs are the foundation: an institution proves a statement — "I hold sufficient reserves," "this counterparty is not sanctioned," "this transaction is valid" — without revealing the underlying data. ZK proof-of-reserves can be published to a regulator on a fixed cadence without exposing portfolio holdings. Privacy pools extend this: a participant proves their funds are not associated with a flagged set without revealing transaction details, separating legitimate confidentiality from illicit mixing. Selective-disclosure viewing keys, proven in Zcash and generalized across institutional stacks, give an auditor or regulator scoped read access while the public sees nothing. Confidential settlement layers (Canton's sub-transaction model, and multi-chain systems like Hinkal that shield sender, recipient, and amount while screening deposits through KYT) complete the set.

The trust model varies by primitive. ZK proofs are trust-minimized — the proof is mathematically verifiable. Viewing keys introduce a key-custody trust assumption: whoever holds the key can decrypt, so key management becomes the control surface. Confidential settlement networks like Canton place trust in the network's permissioning and the sub-transaction privacy boundary. The examiner's first question — who can see what, and under what legal process can confidentiality be lifted — maps directly to which primitive is in use.

Value Flow and Adoption Metrics

The value flow is straightforward: institutions pay for confidentiality infrastructure (network fees, licensing, or protocol fees) and earn the ability to transact on shared ledgers without leaking commercial intelligence. Canton's $4 trillion RWA volume is the headline adoption metric, driven by confidential on-chain collateral that complies with MiCA and Basel III. Hinkal has processed more than 400 million dollars in private volume, a figure whose concentration points to treasury operations rather than retail speculation. Zcash shielded-address adoption rose to roughly 20 to 30 percent of supply, a signal that selective transparency is being used rather than just available. The metric that matters is not total privacy volume but the share carrying compliance tooling — screened deposits, viewing-key provisioning, association-set proofs — because that is the share an institution can actually touch.

Governance, Security, and the Examiner's Questions

A banking examiner evaluating a privacy primitive asks a consistent set of questions, and the primitive's governance and security model must answer each. How is AML and sanctions screening performed when transactions are confidential? The credible answer is screening at the deposit boundary — KYT blocking flagged wallets before funds enter the confidential set — plus association-set proofs, not screening after the fact. Who holds the viewing keys, how are they secured and rotated, and under what legal process can they be compelled? Key management must be documented, access-controlled, and auditable. Can confidentiality be selectively lifted for a regulator or auditor without lifting it for the public or for counterparties? This is the definitional test — a primitive that cannot scope disclosure fails it. How are data residency and GDPR handled, particularly for systems like Midnight that build GDPR-compliant smart contracts? And what is the key-compromise blast radius — the security model must bound what a single compromised key exposes.

Failure Modes and What Is Improving

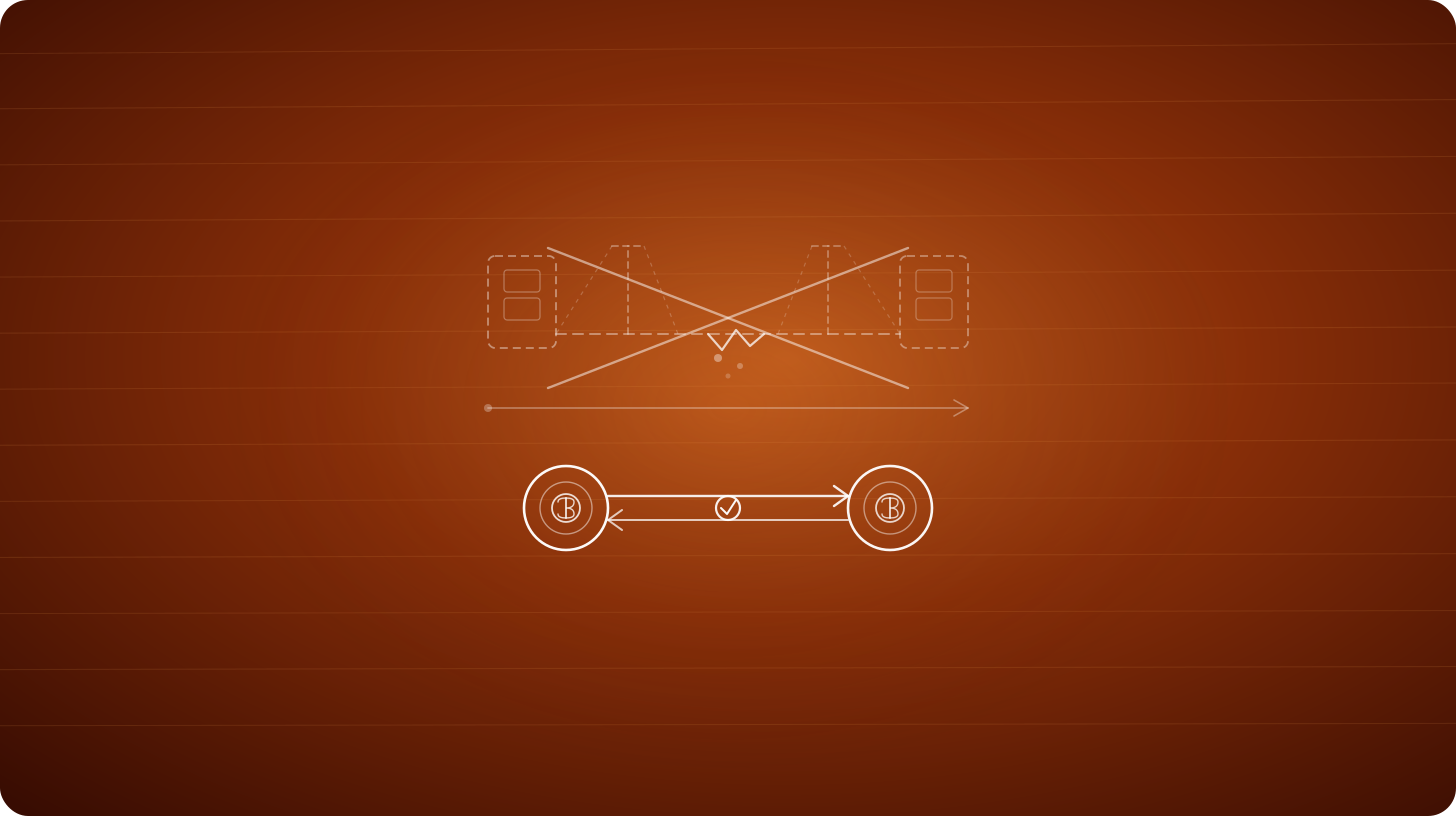

Three failure modes define the category. First, the metadata leak: hiding the sender while exposing the amount still lets competitors map volumes and reverse-engineer commercial relationships, so partial privacy can be worse than none — the mitigation is shielding all three of sender, recipient, and amount, not a subset. Second, key compromise: a viewing key in the wrong hands collapses the confidentiality guarantee, so the mitigation is hardware-backed custody, scoped keys per auditor relationship, and rotation. Third, the compliance-gating gap: a privacy tool without deposit screening or association proofs is a mixer with better branding, and an examiner will treat it as one — the mitigation is compliance tooling built in at the protocol boundary, not bolted on.

The constructive signal is that the regulatory boundary is now legible. Neither MiCA nor the emerging US framework blanket-prohibits privacy-enhancing technology; both target unliftable anonymity specifically. Canton's MiCA and Basel III alignment, Chainlink's institutional privacy standard, and the spread of viewing-key and privacy-pool tooling mean an institution can now select a primitive whose examiner answers are clean rather than improvised. The tools to reconcile privacy with compliance have existed since the 1980s; in 2026 the infrastructure to deploy that reconciliation at institutional scale is finally in production.

For informational purposes only. Not an offer to buy or sell any security. Available only to accredited investors who meet regulatory requirements.